Square Enix: Beyond games

Square Enix faces scrutiny after their latest failures. In this, the first part of a three part series, we introduce the company and review their other businesses.

I don't know who you are, but if you are between 30 and 50, it is very likely you have heard about Final Fantasy. If you are a videogame enthusiast (or have friends that are), Final Fantasy is the king of JRPGs… and arguably of RPGs, at least for a brief period in the late 90s and early 00s1. But even if you are not, dig deep in your memory. Because you probably will remember this:

Final Fantasy: The Spirits Within was a tremendous overtaking at the technical level, displaying the best CGI yet. It was also a complete and utter failure at the box office despite a marketing campaign that pulled all the stops (including a Maxim cover by the CGI lead character). It caused a lot of financial damage to Square and ended the talks of a potential fusion between Square and Enix. Yet it eventually happened.

How Square Enix came to be

Enix was a very profitable company in the 90s but had failed to expand their business outside of Japan. It had a mix of publishing and videogames (with Dragon Quest being their main brand), and the customary Japanese pile of cash. While their current business was alright, they could see the writing on the wall and no path to being global. So they went out shopping.

Square was very different, more adventurous. And it had wild success releasing their JRPGs both in Japan and in the West, especially once PlayStation arrived. Chrono Trigger was already a success, but it was Final Fantasy VII, the first game they developed2 for Sony's console, that made their reputation (and a lot of profit). But they never stopped betting on new stuff, and that came with some wild swings in their profit margins. In particular, the film mentioned above caused a lot of losses and stopped the acquisition talks for the time being. It was, in effect, the death of the old Square.

Yoichi Wada took over as CEO in 2001 after the losses of the film became apparent and focused a lot more on stable profits. Wada didn't come from the gaming industry, but from investment banking, having joined Square only a year and a half before, and took the opportunity offered by the losses to take the leading role at a time when probably being from outside the industry was a plus (as the company was reeling from the film losses). He did squeeze a lot more profit, partly out of luck. Kingdom Hearts, already very advanced when he took over, came out only 4 months later, and it would become one of the mainstay franchises for the group.

Three years later, with Square being now clearly bigger than Enix then, the fusion proceeded, and Wada led the combined group. His reign was lackluster but is the origin of the modern Square Enix.

Why is Square Enix interesting?

Because they own one of the biggest IP libraries in Japan. At first glance, part of the company is underperforming (video games!), part is under-monetized (manga!) and all of seems to be intertwined in too big of a corporate structure. Will that continue to be the case or is there a light at the end of the tunnel?

Square Enix is currently valued at 750B yen (or almost $5B), generated 350B yen in revenue last year, and only 14B in profits, although in prior years it had been around 50B. They have around 220B in net cash as well. So the valuation is not extremely demanding if they can get back to that or surpass it, but it is also not ridiculously low.

Let's have a first overview of their divisions:

Videogames: 70% of the revenues of the company, and their biggest profit source, when things go right. It is further subdivided into HD games (Final Fantasy / Dragon Quest/ Octopath Traveler/ SaGa… main releases and other titles3), SD games (browser and mobile games), where Dragon Quest-derived titles provide the bulk of the revenue and MMOs (FFXIV and Dragon Quest X). The bulk of the profits comes from MMO and SD (MMOs have lower revenue but higher margins), while the HD segment provides prestige and coverage. About 3800 employees in FY 2024.

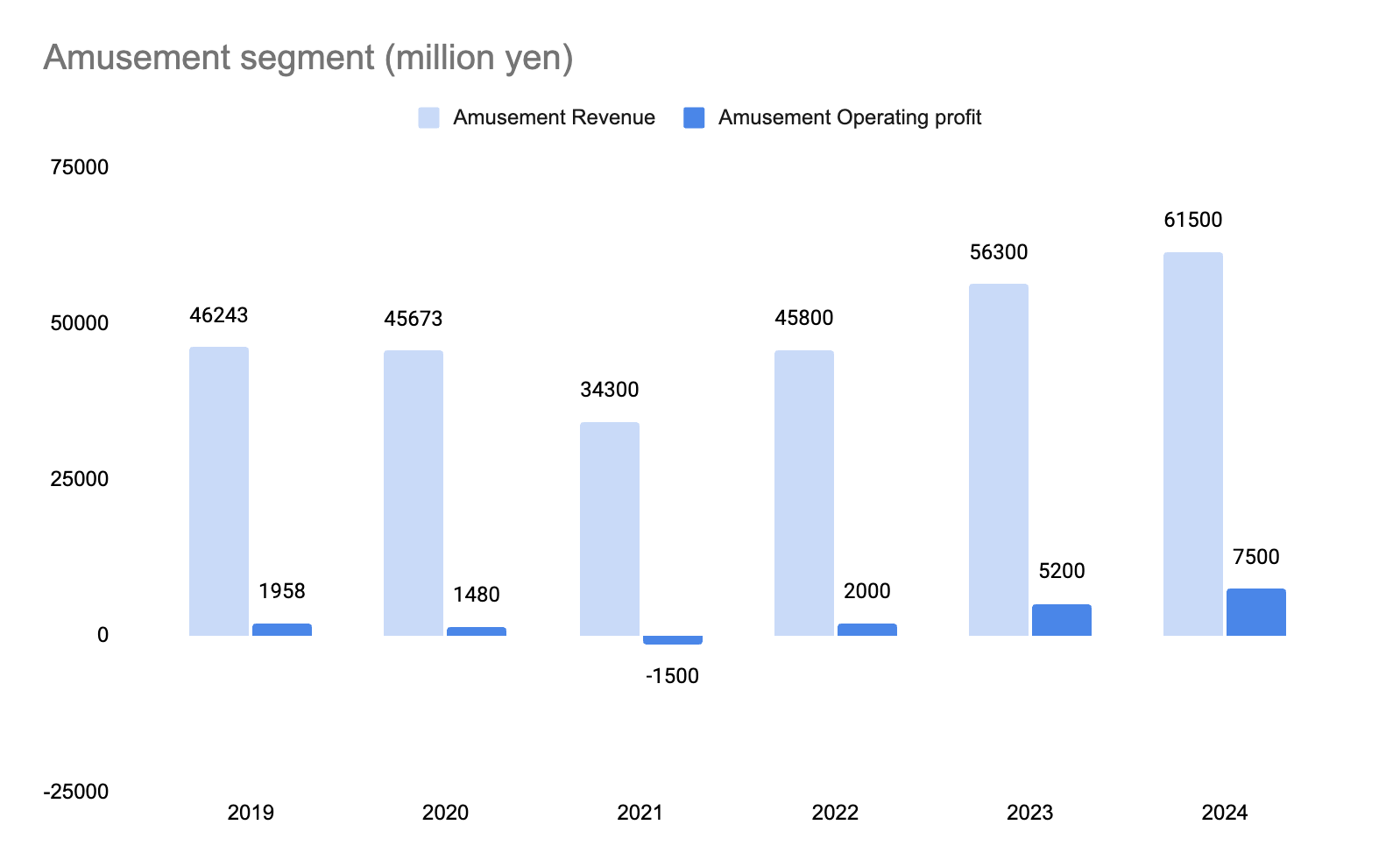

Amusement: Direct management of arcades and amusement facilities, plus providing arcade machines to other facilities. This business comes from the acquisition of Taito in 2005. Used to be a decaying business, but after COVID it is experiencing decent growth in revenue and, especially, margins (reaching 12% in FY24)4. About 2000 employees5.

Publishing: With Enix came their manga publishing branch (and other things, like game guides6). But the important property here is the manga. While the star is Fullmetal Alchemist, and the series ended a long time ago, there are other interesting properties like The Apothecary Diaries or Daemons of the Shadow Realm, and as such they get a participation on anime, merch… made of those series. Consistently, it is the second biggest profit center of the company. It has doubled revenue and tripled its operating profit to almost 12B yen thanks to the success in electronic manga publishing and The Apothecary Diaries anime success7. About 200 employees

Merchandising: Talking about royalties and merch… the royalties they get are booked here, as are their own sales of collectibles (mostly from their own videogames, but also some Sega properties). It has been growing consistently, doing almost 6x the operating profit of 2019 (0.9B) in 2024 (5.6B). 70 employees.

To this, we have to add the corporate structure, which has more than 500 employees and costs about 18B a year.

What I find more interesting about Square Enix is its impressive IP library. It has an extensive manga library, and its videogame IP is difficult to equal, even if it is not managed perfectly right now. I think the value of that IP is bigger than the current market cap, but we have to see how they are doing in extracting profits from it. And it is an ideal time to do so, with a recent change in CEO after a bad FY24 and with a recently presented strategic plan.

I am going to review each of the businesses in detail with their numbers and perspectives. First with all other segments in this part, then in the videogame segment in part two. Then we can go over the new strategic plan, CEO, and how capital allocation is working in recent times in part three.

Square Enix's minor segments

Talking about minor segments here is a misnomer. We are talking about the 5th biggest manga publisher8, a licensing segment that pulls more revenue than, for example, IG Port, and an amusement segment on par with Bandai Namco's and about 60% of Genda's. But they are smaller than the gaming one, and not typically valued when looking at the company as a whole. And I think that is a big mistake.

Amusement centers & arcade machines

Under the heading of amusements, we find two very different segments. One, is the management of amusement facilities, and another is the sale of arcade games and machines to other facilities. Sadly, Square Enix does not break down sales for each.

Overall, the segment has been doing well since COVID, doing record sales and profits in FY2024, with H125 being even slightly better in both sales and profitability. It is difficult to know exactly what is driving the increase there, but my suspicion is that it has two prongs (and it is industry-wide because we see other players benefiting from the trend, like Genda9 or Bandai managing arcades, and Round1/SK10 , Furyu or Sanrio selling to them11)

Better monetization through crane machines and gacha: The sales of what is usually termed prize figures have gone really well in the last few years. Furyu estimates 5% pa growth since 2019 (although they have multiplied their sales by more than 3 in the category).

They are just cool again I guess? Difficult to have proof, but it seems like arcades are getting more popular of late, not less. It is a relatively cheap way to pass the time, and it has the 80s-90s nostalgia pull. Some players are opening new ones (Bandai Namco), others are targeting the US for expansion (Genda, Round1)

Square Enix owns the Taito Station brand. While they operate some centers and others are franchises, it is not clear what the breakdown is for the around 160 centers they have.

In terms of numbers, this is what it looks like. 2024 was a record year with 61.5B yen in revenue and 7.5B yen in operating profit, and H1 2025 is looking even better, with a 30% operating profit increase (on a 27% revenue increase). Since the disclosure is almost non-existent, knowing the breakdown is difficult. I think some of the new stores are franchises (not that much land or machines in the balance sheet despite new openings in 2023-2024, although there is some increase) and expansion12 is partly driving the revenue. I suspect about a quarter of 2024's revenue is machines sold to other parties (including franchisees), but that is based on FY21 Q1 revenue when the managed stores had to be closed because of COVID, so I am assuming most of the revenue there came from machines sold (agreed upon at a prior date). Faulty, I know, but the best indication I have!

This is a business in clear expansion, and stores overseas (only HK for now) seem to be working well. What worries me is that there can be a fadish element to the recent years expansion. I do think stores have a better business model now industry-wide, thanks to the prize segment (gacha, crane…)13 being a bigger part of the mix, and I think tourism helps. But foot traffic might decrease if the nostalgia wave wanes a bit.

In terms of valuation, this is a capital-efficient business (although with relatively low margin), with about 11B yen carried in the books14, and 7.5B in operating profit. Even if we attribute part of the corporate structure costs (say 2B) and consider this is actually 5.5B in operating profit and a tax rate of 30%15, a 3.9B post-tax profit of it is a decent unlevered return on assets (35%), with the capacity to reinvest part of the earnings back into the business at good returns and growing LFL. At the same time, Taito is a recognized brand in the space and Square Enix owns some classical arcade properties (Space Invaders) and a huge videogame catalog that gives them a slight advantage. 100B yen would not be a crazy valuation16 for this business and might in fact be cheap if it is not extremely fadish. You can see Genda, which is only a bit bigger than the amusement segment here, being valued currently at almost 300B yen EV, although part of it comes from the markets loving their aggressive capital allocation17. So for my SOTP (and yes, I can hear everybody groan at the mention!) I am going to stick to the initial number

Publishing

Publishing is more traditional and understandable. What is surprising at first look is that it is… growing? Publishing revenue and profit has more than doubled since 2019, although profits have been roughly flat since FY21.

While it is tempting to think of COVID as the main catalyst here, the trend was already good since 2017, when digital sales started to compensate for the decrease of paper ones.

In the last few years, aside from their sizable back-catalog, they have been pretty good with the things they have selected, and while they publish less series than other publishers, they have been even competing with Kadokawa at times in sales thanks to the success of The Apothecary Diaries18, Daemons of the Shadow Realm and My Dress-up Darling, aside from the already well established Black butler and Soul Eater and their videogame license comics (Final Fantasy and Dragon Quest).

I think there is something going well both in promotion and selection of works in the last few years that is allowing Square Enix to punch well above its weight. It shows in the margins too! Merchandise and IP revenue is not included in this, so it should be fairly lower, and yet we se close to 40% operating margins. Now, expenses are likely to be slightly under-reported (let's remember Square Enix huge unallocated section), and we have to take tax into consideration as well, but their margins are still incredible versus comparables. Mag Garden (IG Port) has a 20% operating margin, and Kadokawa's publishing segment has around 10% margins or below, depending on the year.

What that indicates to me is that Square Enix is winning on selection, not on volume. I don't know if that will continue, but as long as they continue to exhibit this level of good taste, they are going to continue gaining share without having to publish lots of titles.

Let's do the same valuation exercise. Say we take 2B yen of those corporate expenses19 and apply the 30% tax rate we talked about before20. We get 7B yen in profit after tax. Pretty close to cash earnings (barely anything in the balance sheet other than corporate office buildings). Profit growth is a bit less constant, especially as margins have eroded slightly since 2021. Purely as a business, we could slap a 100-150B tag on it and be content with it, but that would not reflect reality all that well.

This segment is the one that generates a good chunk of the IP that then gets exploited in the next one, including money flowing from anime adaptations, which is not booked here. And as we can see, albeit small, that one is growing fast. Guess for our SOTP we can stick with the high end of what I was discussing, but we need to take into account that some of the potential in the Merchandising area comes from here really. Also, the back-catalog of IP (FMA and Soul Eater are the main ones, but there is a lot of depth21) is valuable, and we are seeing that it can trigger interest (see Sony's ongoing attempt to acquire Kadokawa). Oh well, let's slap the 150B tag and be done with it!

Merchandising?

This is a bit of a weird segment, in that the name and the contents match only partially. This segment has Square Enix-produced anime figures (mainly NieR automata and Final Fantasy ones), but it is also where all royalty revenue is recorded, along with anime-related revenue. Maybe that's why that is not the name of the segment in Japanese (ライツ・プロパティ等事業, which apparently translates to Rights, property, and others22 and makes a bit more sense)

Confusing translation choices aside, the business is doing alright

H1 25 has seen a YoY operating profit increase of 80% on a 16% increase in revenue. I don't think the increase will be that big for the full year, but not a bad sign! In this case, the increase in margins in H1 seems to have been driven by the increase in the mix of Masterline figures (or at least that is what the H1 earnings release hints at), which have a price that is a bit unhinged if you ask me

But then again, people pay for it!

It is difficult to get an idea of what the mix is in this segment in terms of royalties versus figures. My impression is that royalties have been increasing steadily, as operating margins have gone from around 12% in 2019 to around 30% (with H1 at a record high 35%). Other players in the industry like Kotobukiya or Furyu regularly record margins around 10-15%, so 30% is definitely anomalous unless rights have picked up23.

For me, this is the most unpredictable segment, maybe because it is an amalgamation of things. Doing the same exercise of attributing 1B of the corporate structure, I think we could easily value this at 50-75B yen, as it has been growing long term (although 2019 is a particularly favorable year for that comparison)

Minor segments wrap-up

When you put all of the minor segments together, you have a business that has multiplied by 4 its operating profit since 2019 and is still growing strongly, with a revenue CAGR of close to 10% and clear operating leverage. The price tag we have put on these businesses is of 300B yen when doing the SOTP business by business, and looking at their recent performance I don't think is a price that is too expensive. Not only that, but in 2019 that evaluation would have been much lower. 100B perhaps? Less?

Square Enix currently trades at a 750B valuation, and 200B of those are, roughly, net cash. The only question that is left to answer is… is the videogame segment that bad? Has it evolved so little, even with the COVID boom, that the evolution of the other segments can't compensate for it?

That is a question that will have to wait for the next part, which will drop in the next few days. Subscribe to avoid missing it!

Update: all parts are now available! You can check them here:

Square Enix II: The JRPG masters

In the first part of this analysis, we went through Square Enix's smaller segments (arcades, merchandising and manga).

Square Enix III: Strategy, allocation, valuation

In the first two parts of this Square Enix deep dive I went through its less well-known segments (manga, merchandising and arcades) , that are doing really well, and its biggest segment, videogames, which is chugging along, with some good things, but with excessive spending in the HD segment, SD declining steeply and MMO relatively stable.

There were good Western titles like Diablo II, Gothic, KOTOR, Neverwinter Nights or TES III : Morrowind. But I think only BioWare (KOTOR, Baldur's Gate, Neverwinter Nights and later Mass Effect) could really compete in both quality and quantity with Square.

They published, but didn't develop, Tobal No.1.

NieR, Life is Strange, Just Cause, Mana, Chrono series… Square Enix video game IP is almost unrivalled, really.

This is not unique to Square Enix. Bandai Namco or Genda are also taking advantage of the resurgence of the amusement centers, although in a different format than before. Collectibles and prize figures are more prominent than arcade games nowadays.

Although only 500 full time permanent ones.

They are even publishing Holoearth Chronciles now, which comes from Cover Corp

No complaints, one of my favorites in recent years! The publication history of this one is weird, with 2 different manga adaptations and

Or whereabouts. Kodansha, Shueisha/Shogakukan and Kadokawa are definitely bigger, their position versus Akita Shoten is variable (they do publish more titles, but Square Enix sells more many months)

Don't miss on Made in Japan's fantastic articles on Genda. 1, 2 and 3

Both pitched by Continuous Compounding - Alan. Round1, SK. We also talked about Furyu together!

Of course SEGA sold at the lowest of the lows for a pittance. I get it, they were not focused on them and it would have required changing them quite a bit to get to anything close to the profit levels other actors have but… well, look at Genda's profits.

2 stores in Hong Kong since late 2023, at least a couple more in Japan, and a new one opening today (plus other one earlier in the month, other 2 in november), so they are going strong at it.

Continuous Compounding - Alan has a decent post explaining how crane games work nowadays

Information obtained from FY2024 annual report, adding up the facilities value listed for the Taito subsidiary plus all the amusement machines value in the balance sheet.

This is the standard effective tax rate in Japan for large companies. Square Enix as a whole pays less currently, but that is largely due to some income being declared overseas, losses that can compensate in other areas... Taito derives almost all its revenue from Japan and it needs to be considered in that light.

25x profits might seem much but they are growing profits at a high rate (40% last year, 30% last H…) and don't need to reinvest much, so this should be close to cash earnings. The only public “pure play" comparable is valued at much loftier multiples on revenue and profit.

Aggressive for a Japanese company, fairly prudent for a rollout by western standards, at least until the last few quarters. Personally I think they are getting a bit ahead of themselves, but they have been masterful operators so far, so maybe they can continue improving profitability. But the more I look into the sector, the more I think they are not as good as operators, they just (not easy!) recognised a sector that was undervalued and turning around. Not sure if that is as good an advantage as being good operators.

The Apothecary Diaries situation is weird, to tsay the least. It originates in a light novel series published by Shufunotomo (a relatively small company) that then has been adapted in two different mangas, one by Shogakukan and one by Square Enix (with the Square Enix one outselling Kadokawa's by about 3x, thanks to the popularity of Nekokurage's style). And the light novels are also published in the US by Square Enix. Production wise, both Square Enix and Shogakukan are there (along with Toho and Nippon TV)

The publishing org is small, with 200 employees, and deeply intertwined with the videogame one (using their IP) and merchandise one (providing IP for them), that's why I suspect they require more support from corporate and assign more than for Amusement, which should be more self-contained.

Here it is less accurate, and we could do 27 or so. But still, let's stick to the Japanese one!

I am going to go out on a limb and be killed for it here, but I think their IP is at least as valuable as Kadokawa's, which gets an outsized reputation because it places higher in the charts due to sheer volume of publications and because, well, Evangelion. But my impression is that a the distribution is very skewed, and a few publications with better average results are a superior model.

Made in Japan was kind enough to double check the automated translation and he was not the only one. Thank you both!

Although Square Enix does not have to pay for most of the IPs they use, so there could be some margin gain there. But Kotobukiya also has figures of their own IP in the sales mix, and although they are able to get to 15% in good years, it doesn't go beyond that. That said, it is worth noting they already reached similar margins back in 2017, although at lower revenue numbers. The Square Enix café (there are 2 now) was cited back then as a big contributor.

Thank you for sharing! Quick math check for the unlevered ROA for amusement business, how did we get 26% ROA on a 3.9B post-tax profit when assuming 11B is carried in the books?

A trilogy! O_O Great start already. Thanks!