PlayWay annual results update

Record results, but record enough?

It is time to revisit again our favorite low-cost game producer1, this time with the excuse of their latest set of annual results and plenty of insights that come with them. But let’s start with the (slightly disappointing for me) headline numbers:

Revenue improved 10.5%, operating profit 15.8% and net profit attributable to shareholders a whopping 59.5%. Still, I expected a bit more in the operational front, with operating profit closer to 200 million than this. The difference largely comes from less profitability in Q4 than I expected as about 35% of the costs of the year have been booked in the last Q, making profitability comparable to that of last year’s Q4 (where the costs of House Flipper 2 were booked) instead of improving on it. While product amortization expenses were indeed far lower than in other quarters as expected, other costs (included some write-offs) concentrated in this quarter, and non-capitalised development services were also accounted for in a larger share than I expected.

Still, full results, even if the sale of Big Cheese is excluded, are excellent, with no major write-downs and relevant income coming from interests on deposits and loans (51% of total financial income). Cash conversion was, as usual, good, with about 160 million PLN in FCF2, and despite the massive dividend paid (effectively 160 million PLN as well) the balance sheet is stronger than ever, with 266 million PLN in cash and deposits and 56 in receivables3, and not many liabilities (60.8 million PLN in total), which leaves us with about 10% of the market cap in current assets. Inventory for PlayWay means completed videogames and work in progress there, that’s why the 103.6 million in inventory should not be taken into account. It is, by the way, a record amount, corresponding mostly to games still in progress (94.8 million PLN).

That is one of the first interesting insights that we can get from this report. PlayWay has not stopped investing, but as was hinted by the reduction in the number of subsidiaries and moves like the sale of Big Cheese and others, they are in a stage of digesting the growth of prior years and focusing in the simulation segment, where they have gotten their biggest successes.

That said, PlayWay’s questions have always been on the future, rather than the present, and that is why it trades at about 12 times profits and with a 7% dividend yield. With that in mind, let’s review the strength of their main IPs, the latest set of releases and their line-up

Main IPs

PlayWay and IP seem antonyms at first sight, but that is a bit of an illusion. While PlayWay’s model is based on throwing a lot of stuff at the wall and see what sticks, from time to time something sticks, and that is a large part of PlayWay’s profits.

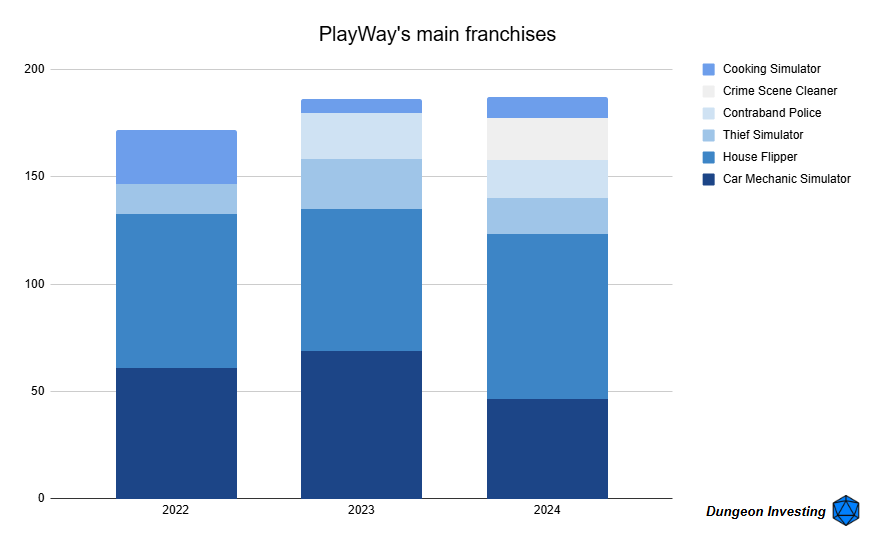

The criteria I have used to include a game or franchise here is generating more than 10 million PLN in a single year since the detailed disclosures started in 20224, and these numbers include DLCs and second parts, in case they exist. A few interesting things:

The demise of Cooking Simulator, a game published in 2019 and that generated relevant revenues thanks to DLCs. However, from 2021 onward, Big Cheese seems to have impoloded, resulting in almost 3 years without new versions or DLCs (from late 2021 until mid 2024) and having the sequel, announced in 2023, still without a release date. These problems ended up causing the sale of PlayWay’s stake in Big Cheese, although they seem to retain publishing rights for the original game.

House Flipper’s continued strength thanks to the release, in late 2023, of House Flipper 2. While not as successful as the original, community-wise, the Co-op mode being released in a few days could revitalise it.

CMS starts to show its age, and especially the slower pace of DLC release (3 in 2024 vs 6 in 2023 and 2022). The new entry in the series (the fourth one) is already in the works, but there is not much information out yet. I initially hoped for it to be released in 2025, given the slower pace of DLCs that seemed to indicate attention switching to the new edition, not so sure anymore!

PlayWay seems capable of generating new additions as evidenced by Contraband Police (2023) and Crime Scene Cleaner (2024). Infection Free Zone (2024) was also a candidate, but is not shown in the list, as it was published by Games Operators and not directly by PlayWay. Regardless, it has seen less consistent sales than either Contraband Police or Crime Scene Cleaner.

Overall, the main franchises generated revenue higher than in 2022 or 2023, thanks to CSC and Contraband Police picking up the slack. The reason I consider those worthy of being main titles despite the lack of sequels is that their sales continue to be strong (Crime Scene Cleaner has sold more than 200k units in 2025 already thanks to content updates and CP more than 100k, and there is a DLC incoming later in the year). But the most interesting thing is not even in there.

PlayWay’s scattershot approach has also meant that the proportion of revenue generated by the big names is smaller this year, an interesting outcome in a right-tail business such as this. Thanks to their low cost, their experiments do, as a basket, pay for themselves and then some, which explains their industry-leading 59% operating margins.

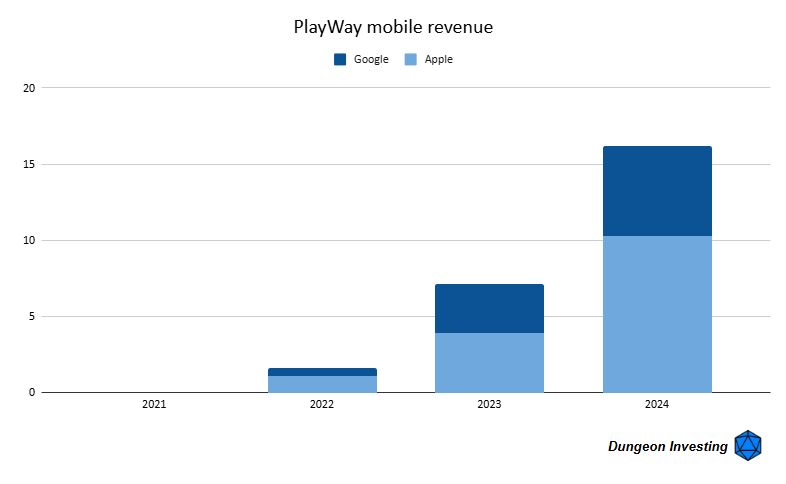

Mobile has been an increasingly important part of this revenue, and seems to continue going up. Mobile-related revenue (as measured by major customers disclosures) has more than doubled in 2024 to 16 million PLN. Still a tiny part of the business, and one at which PlayWay arguably arrived late, but they are growing well at a challenging time for the industry through the release of fast followers, as I mentioned in the last article on the company.

2025 releases so far: between flops and irrelevance

PlayWay’s line-up for early 2025 was never expected to be very successful, and it has sadly failed to surprise to the upside so far. Builders of Egypt failed after its tortuous history of development, resulting in the closure of the studio5, as did Viking Frontiers. None of the other releases was big enough to be relevant, although a few of them (Used Cars Simulator, Car Mechanic Shop Simulator, Chocolate Factory Simulator6) are likely to have been profitable. Some interesting DLCs (Simrail, Gunsmith Simulator, Ship Graveyard Simulator, CMS217) have also been released, but I don’t think it was enough to compensate for the lack of successful new releases.

Pending a couple of releases, Q1 seems like it is going to be slower in terms of sales than last year, and Q2 looks that way so far, at least in terms of revenue and pending some releases (Survival Machine and the CoOp DLC update for House Flipper 2). I expect profitability to be mediocre for PlayWay as well, as some games (Builders of Egypt, Haunted House Renovator) had relatively relevant budgets8.

The line-up

There are some interesting releases coming right up, as mentioned. Survival Machine (today!) is the one that looks better so far. Wrap House Simulator (no date but scheduled for May, potential delay) is a bit of a dark horse, with the demo having surprisingly good peaks and reviews, but translating into less following and wishlists of the main game than I would like. But the big one is the House Flipper 2 Co-op, coming up on the 15th of May. If it manages to revitalise the House Flipper community, this can make not only the quarter, but the year for PlayWay. House Flipper 1, 2, and DLCs amounted to 25% of total games sold last year after barely slowing down from 40 in H1 to 37 million PLN in H2, so keeping it fresh is vital for the company. Conversely, a failure there would be really bad for the company, at least in the short term.

Beyond the immediate releases, the most interesting things remaining but without confirmed release dates (although most are aiming for 2025 officially) are the same as discussed previously: 30 days on ship, Holstin (both in Steam’s top 100 wishlists, although toward the end of it), and Honeycomb9. The star is, however, the new iteration of CMS, and I don’t know when it will be released.

Additionally, there are very interesting upcoming DLCs. Aside from future content for House Flipper and CMS21 (as of yet unannounced, but I have no doubt it is incoming10), there is new content upcoming for Gunsmith Simulator, Thief Simulator 2 and, in Q4, Contraband Police11.

Conclusion

As always, backward looking results are not really what is more interesting here, as good as they might be. PlayWay trades cheaply because it is really hard for people to get behind a videogame company without premium IP these days. But it seems like the shotgun approach keeps delivering results, as long as costs are kept in check.

Personally, seeing what is pending I think PlayWay is still well positioned, with 3 really strong titles in the line up (new CMS, 30 days, Holstin) and an upcoming slate of content for their key titles that looks fairly attractive.

More importantly, I think that the future of games is a bit of a barbell, with very disciplined low-cost, low-price operators on one end and the GTA VIs and Baldur’s Gate 3’s of the world in the other12, and I haven’t seen any operator more disciplined an committed to the low-cost approach than PlayWay, combined with a preference for returning money to shareholders rather than empire-building, so a 13.5x13 multiple on 2024’s EBIT, that I think is likely to improve in the near future even if H1 2025 is soft, still looks cheap to me, especially coupled with a strong balance sheet.

As always, please do your own research. And if you want to leave your opinion in the comments, hey, that’s what they are for!

Miscelanea

IG Port also presented results! Better than expected, but according to management that is only a timing issue (with their Q4 expected to be weaker). While their revenues are up 32% and their operating profit 47%, their net income is still down 11%, as the difference in tax rates I mentioned last time is still affecting them (aside from some other operating income last year related to investments). They have also announced a lot of new series, aside from continuations of their strong portfolio (Spy x Family, Kaiju n. 8, and the upcoming One Piece remake):

A Star Wars series (and two shorts) for Disney+

An adaptation of Agents of the Four Seasons, where they are taking a big part in the production committee.

A new Haikyuu!! movie

A new series for Netflix with Sanrio characters

And more, too much stuff to list!

I’m back being a shareholder of both Cover and now also of Anycolor, as outlined last time. Cover’s hit on Gura leaving was smaller than expected, so you probably did better than me if you didn’t trade around!

Who said a shadowdrop can’t work? While it hasn’t quite ruined Clair Obscur: Expedition 33’s debut, TESIV: Oblivion Remastered has been one of the most successful releases of the year so far, with more than 2 million copies sold in Steam alone, according to estimations. Given that it is available on Game Pass and on PlayStation as well, that impact is very likely to be underestimated. It currently ranks second in Gamalytics estimated revenue for this year’s releases, only behind Monster Hunter Wilds (although practically tied with KC:D2, R.E.P.O., and Schedule I). The impressive part is that there was no marketing campaign14, and the announcement and release were simultaneous. With rare exceptions, timelines from announcement to release have been shrinking, and I see more and more reliance on shock and awe over letting fans marinate with drops of information from time to time, as used to be the case. It might be a reflection of our shorter collective attention span, of the saturation of the market (more difficult to keep the attention of your potential customers for a year with 10 good releases for the same public going on in between), or any other thing. My impression is that, except for rare exceptions, revenue generation also happens in an increasingly smaller timeframe, with rare exceptions15.

With Nihon Falcom’s permission!

How is that possible if they had only 153 million in OpCF? Well, even not taking into account the sale of shares in associates as positive in this regard, they did receive other 17 million PLN between interests and loan repayments that far exceed the 6 million in investments. The negative 29 million PLN in other investment flows is largely related to the effect on consolidation of the sale of shares, so I am not taking it into account here. In practice, FCF is slightly higher, and they got other 47 million PLN from sales of shares (which I don’t include in the calculation). As you know, FCF calculation requires some judgement, so do your own!

Mostly from Steam and other platforms, so credit risk is negligible. 5.9% of them are overdue, up from 4.7% last year. This year’s total credit write-offs were 1 million PLN, and 5.6 million PLN in the company’s lifetime. As a note, total amount of provisions actually went slightly down this year, as reversions were bigger than additions. PlayWay tends to be pretty conservative accounting wise.

PlayWay has always been more transparent than average, but before 2022 the detailed disclosure was made in terms of units, not revenue generated. While that disclosure is still present, it is less relevant in terms of comparisons so I preferred to go with revenue comparissons.

No surprise that PlayWay chose to close the subsidiary as soon as they could, as the main developer had complained frequently about PlayWay and public comments by PlayWay’s CEO were not particularly nice either. It was a mismatch on what they expected from the other side from the beginning, not just that the game didn’t do well - which was to be expected after the lack of communication and constant delays.

No one said you had to be imaginative to name these games.

Though let’s face it, the Taxi DLC has performed poorly.

For Playway. That is well below $1 million per game. Haunted house was between 1.5-2 million PLN in my estimation, BoE probably 2-3 million PLN.

I am Jesus Christ is still in there somewhere I guess, but it was announced in 2019 and at this point, even if it is released, I expect nothing from it, in a somewhat similar situation to Builders of Egypt. FWIW, there are still dev updates from time to time. But this is the kind of game that needs a fast release after going viral, or the joke goes old FAST.

The latest CMS21 DLC was announced with 2 months of notice, latest House Flipper paid DLC was announced with one month, and the release date of HF2 Co-op was announced only days ago, with about 2 weeks to go. Marketing timelines are shortening in general with even some relevant games (like the Oblivion remaster) being announced on the day of release.

And a powerwash DLC for Prison Simulator. Hope they don’t get sued!

With some exceptions, which are the ones I am more interested in. I think there is space for Creative Assembly, Paradox, Atlus, RGG and some version of Square Enix in that world, as long as they embrace and cater to their captive communities.

Wait, but PlayWay trades at 11x EBIT… Ok, you got me. I adjusted it for the minority stakes, taking out roughly 20% of the EBIT. I prefer to use that adjusted EBIT rather than profits because of the sale of Big Cheese… but look, the relevant part here is that they are still paying hefty dividends and will continue to do so because they generate the cash flow for it.

Well, almost. Part of the specialised media knew and had review copies, from what I’ve heard, and there had been leaks swirling around for a while.

Happens with some year-defining games (Baldur’s Gate 3 rarely drops from the top 100 a year and a half after release, and the same goes for Elden Ring or Cyberpunk 2077). Also happens to a lesser extent with games with a very loyal following that keeps promoting them. Persona 5: Royal (and the entire Persona franchise to some extent) or NieR: Automata are some of the key examples, selling above rational expectations year after year.

Interesting. Why do they pay out such a high share? Isn't that a bit too much?