Toei Animation or Toei Company?

Toei Animation has all the interesting stuff, but Toei Company allows you to buy it at a discount. Or maybe bet on it in a different way?

Toei Animation is expensive. For relatively good reason though! They have essentially tripled revenue and quadrupled their results since 2016. I used to own them in 2020, but I was unable to bring myself to buy again in the 2022 drop.

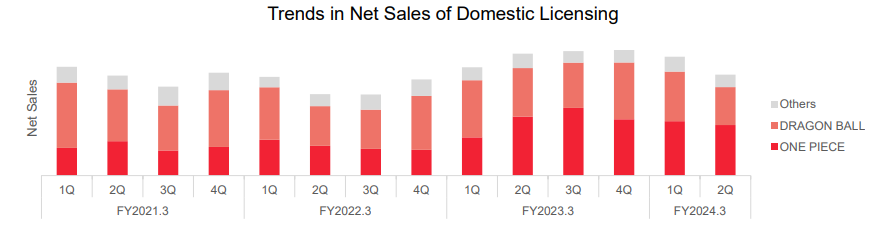

In all honesty, I thought it was a bit richly valued, and that they hadn't that much room to grow. Well, I was wrong. Not only Dragon Ball & One Piece are the gift that keeps on giving (both growing their overseas licensing and film revenue, and One Piece even growing its domestic licensing one), but Toei Animation depends a bit less on them than a few years ago.

In 2020, Dragon Ball and One Piece represented more than 54% of Toei's total revenue (since they don't disclose the domestic film share per franchise, that part is not included). In their last half-year results, the same calculation rendered only 44%. Toei is still unable to come up with good new franchises, but they have been skillful in milking Slam Dunk, Sailor Moon, Saint Seiya, and Digimon.

That said, at about 45xFCF, I don't dare to own this. Being the gateway drug into anime-related stocks has its price, but it is not that high. Not to mention that, while it is is still a very good business, it is right off the heights of The First Slam Dunk and One Piece: Red. Not all anime films are that successful. But the valuation spread between Toei Animation and its parent, Toei Company, has been growing quite a lot of late, and I think it offers an opportunity. Toei Company owns about 40% of Toei Animation, and its market cap is below1 the market value of that stake2. And Toei Animation is far from the only thing Toei Company owns.

Toei Company

Since the possibility I am looking at is shorting Toei Animation and longing Toei Company to bet on a compression of the discount. What brought it to my attention was this article shared by Teddy Okuyama on X which included, among other things, this graph:

And well, we are not in November anymore, but the situation is similar, with Toei Animation at historically very high multiples and Toei Company at slightly below the value of their stake (at about 90% as I write this, which would be more than understandable if it was the only asset in Toei Company).

So let’s look into their other assets. First, let’s look at the rest of the shares they own. Let’s keep in mind there should be a decent discount here, as Toei Company has not disclosed any plans to sell their cross-shareholding in any way! In their balance sheet they record ¥33B in public stocks, according to their latest annual report. That, however, does not include their Asahi stake, which is consolidated through the equity method. Taking it into account I get, with updated values as of today:

That is, about ¥50B3. Other shares in there are valued at least at ¥5-6B more, but this is the lion’s share of the portfolio.

Then, there is the cash and investments part of the balance sheet. Which is not that much. ¥30B in cash once you subtract Animation’s hoard. Stock investments seem huge in the balance sheet, but part of it comes from the valuation of the stakes in affiliates in there (since variation goes through other comprehensive income). And you have to subtract about ¥15B in debt.

And then there is Toei Company’s business, which is mostly making films and TV shows and licensing it for toys and the like if they can (Super Sentai), although they also have some involvement in tourism, events and real state, and a cinema chain. The TL;DR is it isn’t a fantastic business (7,5% net profit margin in the last half), but it has regularly produced profits, even through the pandemic (even if greatly reduced)

Last year it was about ¥7B, this year is going worse so far, but still profitable enough (with ¥3B in profits in the first half). Due to the capex-heavy nature of some of their business, cash conversion is lumpy and not as fantastic as for animation ( ¥4-5B in a normal year I think, although the COVID years were negative).

Not a great business, but easy to talk about ¥50B of valuation.

So all in all, with stocks, cash and the business, we are talking about ¥115B of “fair value“ so to speak, certainly not below zero, which is the actual implied valuation right now.

Why now?

Well, as I said, Toei Animation has gotten ahead a little bit in terms of valuation, and faces very, very tough comparables. That happened once already, back in 2021. As growth stalled for about a year, its valuation came down to Earth a bit, especially in early 2022. Toei Company mirrored its subsidiary of course, but much more subdued. While the parent lost about 27% from peak to through, for Animation it was about 67%.

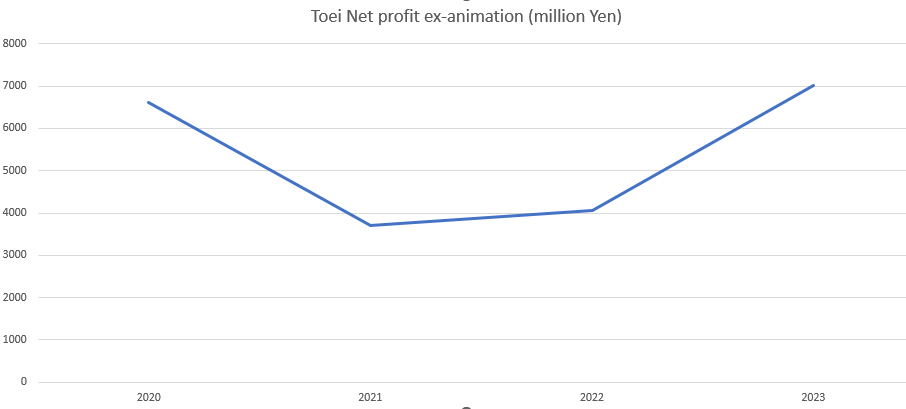

Now, that might not be the same right now, but I think Toei Animation is also looking at another plateau, or even a slight decline, in the following quarters. At least that is what it’s looking like right now:

Overseas film income is looking incredible, to be fair. But my impression looking at their forecasts is that is not going to hold and it was pretty lumpy. Current predictions from the company set profits at about FY22 level. I don’t think that is going to be the case (Toei Animation famously always sandbags) but last year’s forecast at the time was quite a bit higher, and there were reasons to think it was going to be even better.

So what I think is that, overall, the multiple will compress in Toei Animation, and Toei Co. will react far less.

There is another possible catalyst here, which is that Toei does something to facilitate listing status, as Toei Animation probably does not have the float to comply with the standard segment rules. If that were to happen, Toei Co. should see a raise in value because it would be either by doing a spin-off of shares to its shareholders or selling the stake (or part of it) for cash. But in all honesty, I am not counting on it. Toei Co.’s management has not disclosed any plan in that regard, there is a lot of time to comply with those requirements, and exemptions can be granted.

I am also not counting on a bidding war for Toei Animation in the style of the Pasona/Benefit One situation mentioned in the first article. Toei Animation is bigger (although Benefit One is also richly valued). And, in all honesty, I am not sure what that would do to the discount. Animation would go up immediately, and I am not sure what would happen with Co.’s shares (I mean, it would be a Japanese company with a pile of cash).

So yeah, it is a bit of a risky bet, as (almost) all pair trades are.

But honestly, I would gladly go with it, if Interactive Brokers allowed it. Sadly, Toei Animation is not amongst the Japanese stocks you can short in the platform (Toei Company is).

So if anyone knows about a platform that allows it, please tell me!

Of course, do your own research, this is not a recommendation, only the frustrated musings of someone who can’t make the trade he wants.

I know if you check Google Finance it is slightly above, but that doesn’t take into account treasury shares. That means Toei Company’s market cap is ¥260B instead of the ¥299B set by Google, and Animation’s is ¥710B instead of 730. That is pretty common with Japanese stocks, so beware!

And then there is TV Asahi Holdings Corporation, which owns a sizable stake in both, and is also valued at about 60% of their equity portfolio, with a sizable cash position and a profitable business on top of it. Cross-company shareholding in Japan is so, so funny. But I don't see a catalyst on this one.

This does not include Toei Animation’s stake in Bandai Namco, of course. Cross'-shareholdings are a nightmare