The Old World, IG Port, Beer Factory, Paradox Price Hikes

A quick review of some of the latest news in the hobby market, and some other oddities

The Old World is out (of stock)

The Old World is out, and Games Workshop ran out of inventory. A pretty classic tale that I thought we had left behind in 2021. It is not entirely surprising. On one hand, square base games have been out of their portfolio since 2015, so it was difficult to predict demand. On the other, Games Workshop has been treating TOW as a sideshow pretty much since it was announced, and it seems like their production schedule was modeled the same way.

I don’t entirely blame them for that. WHFB was a lousy seller in the last years of its existence. It was also never popular in North America, that now represents about 41% of their sales (versus 26% back when WHFB was a thing). Those preferences seem to hold true, and Europe was out of stock faster, and also for both factions, while the American side still has a few skeletons for sale.

I do hope that this first test has given them a good idea of what to expect going forward, and how much effort should be put into this line.

On a more positive note, Games Workshop published its H1 report. As we knew from December, margins in the full H1 were not quite as extraordinary as in Q1. Q2 was slower than Q1, and down sequentially, but that was only to be expected1. It was still 7% up YoY. But the composition of the margins is, overall, good news.

Gross margins are up to 69%, best since 2021 and back on historical grounds after two relatively lousy years (67% and 66%2). Part of it is the reduction of shipping costs and less inventory write-down, and then a bit of operating leverage as sales went up. That was something I expected!

Operating margins are also up, but only from 33 to 35%. I did expect more! But looking at the reasons (major IT projects and increases in pay and increase of staff both in manufacturing and design) I am not particularly concerned. I will be concerned if the major project expenditure is not reigned in a bit, but looking at the cash flow statement, it seems like it is. Which brings me to…

Cash flow generation is up big time. 26% in FCF, once you take out investments and leases. A combination of less expense in capitalized major projects and a slight decrease in PP&E, plus WC reducing very slightly. In all honesty, capital efficiency is something I would prefer GAW to focus a bit less on. Once you strip cash and intangibles in the balance sheet, their ROTE is above 100%3. Mr. Rountree, if the next marginal pound of investment only gets a 50% yield on that basis, please do invest it, I am not going to get that if you give it to me as a dividend.

IG Port results are out

And the market didn't like them initially, punishing the stock with a 6% fall! Their 40% increase in net profits and 25% in operating profits was not enough to cover the market’s expectations. Perhaps because it comes together with revenue down 7%, and that is not something that is allowed for a “growth” company. Except they grew the important segment (copyright) far more than required, and profits are way up. So after thinking it over the weekend, the market sent the stock up 15%.

The main reason for that lack of top-line growth seems to be the release schedule. IG Port is behind the production of several manga and anime hits (Attack on Titan and Spy x Family are probably the most well-known ones, along with Ghost in the Shell for the old among us), but their revenue has a very different composition than that of TOEI, mostly because they haven’t had any generational success (but also because of how their licensing is structured4). While TOEI gets most of its money from royalties on toys, merchandising and videogames, IG Port gets less than 12%5. Still, it does make around 20% of its revenue on a combination of royalties and existing work, and it should have increasing margins (as the corpus available expands and IG Port is able to get better deals, hopefully). It already moved from 15% in last year’s H1 to 20% now.

As I was saying, they mostly depend still on the anime and manga they are publishing now… and they have interesting projects coming. The One Piece and the Suicide Squad anime adaptation are projects where I don’t expect them to have a strong share of royalties in terms of merchandise and so on (obviously yes on re-runs and international runs). But Kaiju n.8 and Spy x Family… well, there are reasons to believe!

All in all, it might be inexpensive for the potential it has at about 20x earnings and the customary Japanese cash hoard. Might do a deep dive on it, let me know in the comments if you are interested!

Videogame medley

The start of the year in the video game market has been a bit sluggish. None of the new entrants has been able to hold on to the chart long enough to appear in SteamDB’s weekly best-sellers. The rest of the month is a bit stronger, with Three Kingdoms: Zhao Yun, Like a Dragon: Infinite Wealth, Tekken 8, and New Cycle. But that doesn’t mean there was nothing interesting to see in the sector!

First, Paradox announced an increase in their subscription prices for HoI4 and EUIV with a 6-day notice. A bit sneaky, especially when it is a 60% increase! Given that Cities Skylines 2 sits at around 60% positive ratings and has about the same concurrent users as the first iteration and Victoria 3 also didn’t quite live up to expectations… not sure they need the flak they are going to get. But they probably need the money. To be honest, this is a company I love and I have faith on them eventually recovering. I have never understood their stock price though.6

And second, PlayWay launched another of their small games, Beer Factory. And honestly, it was interesting to watch. The launch started really well, with more than 2k CCU (which, for a small-budget game, is a lot!). Then, bug reports started coming in. Even positive reviews mentioned the bugs. So naturally, this game is a financial disaster now, right?

Wrong. It is easier to recover the costs of a game when they are about $75k.

That said, kriswawa, please7, try to spend a bit more on testing or supporting individual videogame developers like this one when the game has a bit of promise. Based on the response to the despite the fact that it was unplayable, PlayWay has probably lost the opportunity to make a couple million there.

Sad8

Shootout corner (and some house-keeping)

As you probably have noticed, this is the second “news“ article I send your way. I will be doing this type of publication every 2 weeks, because I think it still brings some value, and allows me to publish with some frequency while still having time to work properly on stock-specific articles. Let me know what you think!

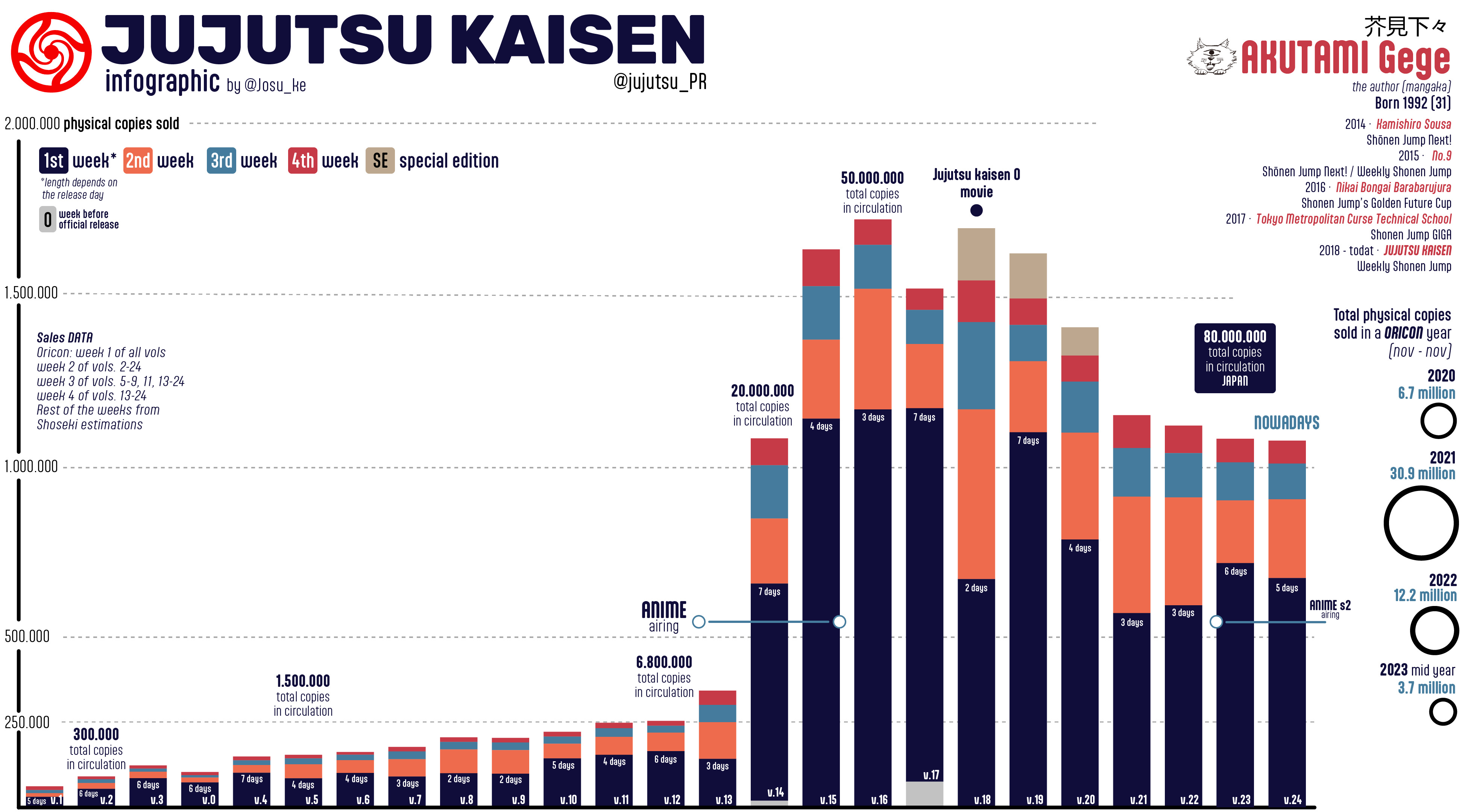

But while I do them, I want to use part of this space to talk about people that are making my life easier with their tools or their content. Today’s choice might seem a bit random, as it is not strictly investing… but it is very useful to check Japanese content trends!

Josu_ke is a manga-obsessed graphic designer from Spain. And he publishes what I think are the best infographics about the manga market. His web, MangaCodex, is a must for anyone interested in the market, and has infographics per series, weekly data summaries either there or in X, access to compiled Oricon data, an all-time manga top seller ranking… just look at the Jujutsu Kaisen visualization

By the way, I have never talked with him, so this is as far from a paid endorsement as you can get. Josu_ke just does a fantastic job and I check it often. Now, you can too!

Leviathan launched in Q1

2023 was the worst year (in terms of gross margin) in more than 20 years. You have to go to 2002 to find a worse one, and it was 66.3 instead of 66.5.

You have to be careful when excluding cash. Some level of cash is actually needed to operate many businesses. If we were to include GAW’s stated cash buffer, then its ROTE is “only“ 81%. The buffer is a bit over-dramatic as it is calculated on “money we need to cover all our usual expenses without receiving a dime from customers or taking a loan”. But hey, better overcautious than over-levered.

MBS was in control of the anime, not IG Port, and that’s why it changed hands in season 4. They don’t get most of the licensing revenue, or their copyright segment would be much, much bigger. I suspect the same holds true for their One Piece remake and others.

Much less. It is uncertain how much of the distributions from production committees come from that and how much comes from audiovisual royalties, but 12% would be if the full amount came from that.

They have grown revenue 3x since 2016, and that is great. Accounting profits are up pretty much the same, showing no operating leverage. Cash conversion is a bit worse, because they have been investing heavily in new games. Not the kind of business I want to buy at about 50x LTM FCF.

I know this is mostly under CreativeForge, but come on, you can talk with them!

As a shareholder, I am, indeed, very, very sad!

Hey There, i enjoy your approach a lot. IP investing is one of my favourites.

Would love a deep dive on IG port.

Keep the good work

Cheers!