Sega Sammy (6460.T) 2024 results update

Sega Sammy's results have been well received and come with relevant strategic news.

After the annual results for Sega Sammy were published on Friday the stock has proceeded to surge by around 10%. That comes on the back of both strong business performance after lackluster guidance and, I think, an appreciation of some strategic changes the company has communicated.

Better results than expected, but lower earnings?

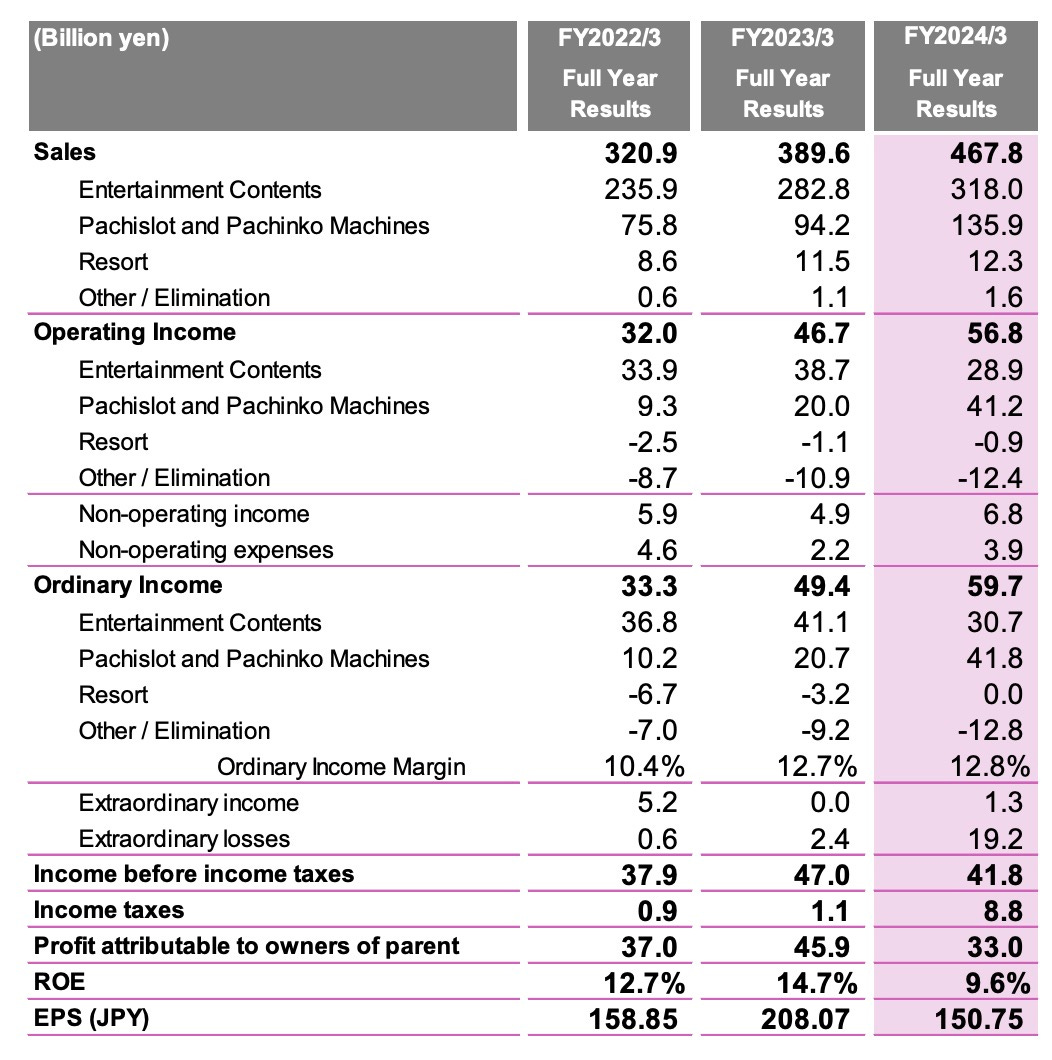

Almost all the games subsegments did as expected or better, except for Rovio, that continues in free fall. The new games part managed to live up to expectations. Given that expectations were that it was to be their best quarter in many years on that front, great! What was not expected was the fantastic performance of the back-catalog (almost 40% above guidance issued in February for the quarter). I suspect Persona 5 Royal had a lot to do here, given that the geographical mix is more Japan-oriented than usual and I saw the Persona 3 Reload release re-ignite interest for the game. Of course, none of those are really news (I already went over the LAD8 & P3R strong releases a few months back)

The improvement is not currency-depreciation driven, although I am sure it helped. Overseas sales represented 73% of game sales, the lowest quarter since 2020, so it was mostly just great performance in Japan (and also the rest of Asia). F2P in Asia also went better than expected, about 10% above forecast in the quarter and reverting its downward trajectory, and Anime did better as well.

One thing of note is that profitability improved a lot more in the segment than initially expected… but at the same time extraordinary losses increased a lot, mostly because Relic was sold1. That in turn caused overall profits to be actually lower than initially predicted, as the business was sold at a lot less than it was marked in the balance sheet.

In the Pachinko business, the latest forecast was spot-on, with low sales during the quarter in both Pachinko and Pachislot. On this, I was wrong, as I thought they would be slightly higher than the outlook mentioned2. Not that it matters to complete the best year in sales since 2020 and, more importantly, the best in terms of profits in a decade. As I laid out in my initial write-up, Pachinko & Pachislot are being run in a more streamlined way and as a cash cow, and that is noticeable.

It is also being run with a focus on slot machines vs. pachinko, which should slow down its ultimate demise (as it declines far slower, and has actually gone up after bottoming out in 2018. Sega is now at 21.3% utilization share in Pachislot, and has, as I write, 4 of the top 253 machines per installed base in the country, according to p-world. In Pachinko de situation is very different, with timid efforts to regain share there so far not resulting in much.

All in all, ¥33B in profit, and about ¥49B in free cash flow4. Pretty healthy! The result announcement was accompanied with an announcement of a ¥5.8B year-end dividend (to be added to ¥5B in the interim dividend) and ¥10B repurchase to be conducted along the whole financial year. As a reminder, Sega Sammy stands at about ¥500B of market cap now, so that's a 4% yield. Which is OK-ish, but not great value territory, unless one thinks results will still go up in the coming years. And to understand that, let's get into the important stuff in this earnings release…

Resorts are out, international gambling is in, videogame reform

Phoenix Seagaia has been sold! That will bring a relatively modest gain on sale (for Sega Sammy's size) of ¥8.5B, and they will keep 20% of the new partnership with Fortress, so no more focus on resorts, even if they keep participation here and in Paradise. I am really happy to see a more focused company.

Well, focused is perhaps too strong a word, because they are adding a new area inside Sammy, called Gaming which includes:

Online gambling (if they acquire GAN finally, I guess, although they have some small initiatives in Japan)

Sega Sammy Creation slot machines (that is, international sales of slot machines). Incidentally, they have revealed this only brought ¥2B in sales last year

To that, we have to add the changes in the entertainment contents area, with animation now being independent of toys and amusement machines which are now under the same entity.

And last but not least, the Relic sale announced a month and a half ago. We still don't know the exact terms, and we might not for a while, especially if the cash movements are not in the same period, but I don't expect it to have been high.

This is pretty weird for me, but of all this I only dislike the online gambling part5. Slot machines make sense. They already have the capacity and the expertise, and they know it will probably become underutilized in the future, so making an effort to try to use it for other markets makes sense. I don't know if it will pay off, but Light & Wonder (former Games Scientific), market leader, trades at twice Sega Sammy's entire market cap. And that means there is more than enough market, even if the established players are difficult to dislodge… and the cost of trying to enter for SGAMY is not the same as for a newly established player. I like it so much that I called it out as the biggest avenue of potential growth for the segment in the original write-up.

The changes in entertainment are not just reporting changes to highlight TMS vs. the Toys and AM area. They also put Toys and AM in a single segregated society in what, to me, sounds like preparation for yet another divestment… which is music to my ears. Quoting my prior write-up:

The machines sell well, but it is a very low-margin business that I hope they get rid of someday (although it is generating ¥4B in operating profits a year). The toy business is, I think, too small nowadays to be very profitable, and they would probably be better off working with other toy companies instead.

As for Relic, I am happy it was sold. The studio did not fit in Sega's strategy of series IP creation and exploitation, I think, although CoH might have. Quoting myself again (at the risk of sounding like an egomaniac):

Relic… I honestly don't know what I would do with that studio. They are sort of specialized in RTS, but they are very hit-and-miss within the genre. Dawn of War III was terrible, AoE IV was good, CoH III was terrible. I don't see how they can make money with that hit/miss rate on pretty expensive games (especially given that the only relatively recent success was a contract job). I hope things change, but right now, I would be glad if it was sold.

And then there is the European re-structuring, where European seems to be a code word for Creative Assembly. We haven't heard much in terms of changes in Amplitude (although I suspect there have been some), Sports Interactive (no), or Two Point (I don't think so!). In terms of Creative Assembly, the word seems to be full focus on Total War, and they are doing pretty well with the latest DLC sending TW:W3 into the top 10 steam best sellers again and with the biggest CCU peak since 2022. Let's hope their content strategy keeps hitting the nail in the head, and that the next announcement for the series also come soon (no, Pharaoh does not count).

All in all, Sega seems to be running almost the same playbook I would choose (well, I would try to get out of the GAN deal, but I don't think they will). Color me happy!

What to expect in FY25

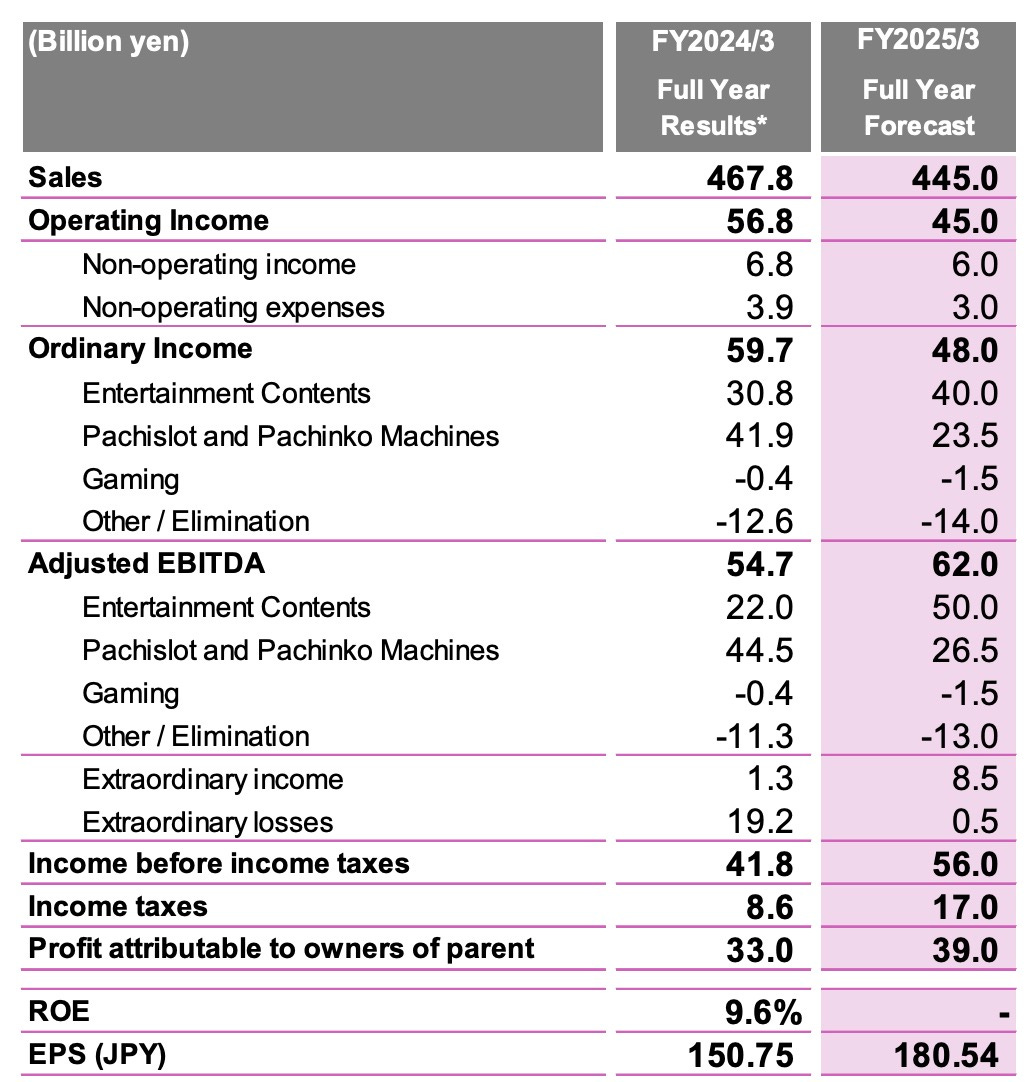

FY25 Guidance was OK, but not much more.

It is a lot softer on Pachinko/Pachislot, but that's because they don't predict any super-hits this year. Smart guys. This year's success is difficult to achieve. The international gambling one reflects only that there will be a bigger investment in the area. Entertainment though… it seems soft to me.

They expect slightly lower main game sales and higher of back-catalog, and a small increase in F2P. But the lion's share of the increase in sales comes from Rovio being consolidated for the full year. They expect only 2 new F2P titles to be launched (unclear to me if P5X is counted there) and 8 full games (at least 4 of which are already known)

In general, in terms of videogames the playbook seems to be:

Bank on the strong Japanese IPs with relatively frequent but cost-controlled releases and a big one from time to time. Sonic is an example (Sonic Frontiers is the last really big Sonic game). Persona is another, perhaps clearer. Major versions are very spaced (Persona 6 release date is rumoured to be in 2026, 10 years after Persona 5), but Persona 5 has had a more complete version (Royal), a remaster of Royal, 3 spin-offs and a mobile game (just released!). What we have to look forward in this regard for this year is

Shin Megami Tensei V: Vengeance

Sonic x Shadow Generations (expected to be released at almost the same time as the movie)

Metaphor: ReFantazio (a new IP spawning from Atlus studio)

Although I include here the recovery of old Sega IP, it doesn't look like any of those releases will happen in 2024.

Limit the worst excesses of the COVID era in the European segment, and refocus each studio in its core strengths, and at the same time, don't touch what is working (that is, Sports Interactive, where Football Manager is killing it). What do we have to look forward to here?

From SI: Football Manager 2025, the first release with a new game engine. I expect it to do worse than 2024 because major updates in the series have always been rocky, and this is the biggest one yet. Also, 2024 being the strongest release in the series.

From CA: New DLCs and content for Total War: Warhammer 3. If they keep going like ToD, this will be a major source of profits again.

Not sure what Amplitude and Two Point are cooking. But Two Point never really strayed off its casual-simulation space (with Campus DLCs being their only releases for a while now). Amplitude is a different story, and I am honestly intrigued.

Use Rovio's mobile expertise in combination with the Japanese IPs to increase their footprint in mobile. Sure, Sega Sammy has a solid F2P business… but only in Japan. And their IPs are stronger than that. What we have in this area is:

Persona 5: The Phantom X - Decent, but not stable, start in Taiwan, Macao, Hong Kong and South Korea. The game initially started out making great numbers (top 1-5), but a month later it has fallen into positions closer to #100, let's see how the international releases do and how stable that position is (if it stabilises there, it can be pretty profitable). This game is not developed or published by Sega in most countries, they only get the licensing rights, but it was still called out in the earnings release.

Sonic Rumble: fallguys-style game with Sonic characters that will launch by the end of 2024 (coinciding, again, with the film). First Rovio collaboration

It is a good strategy I think. Coupled with the Sonic 3 release and the different series, It has potential for good licensing and F2P revenue outside of Japan. And it is clear they are counting with decent launches for Metaphor and Sonic x Shadow, but not incredible ones (as they count on 9 million units sold total of new games between all 8 releases), and F2P revenue outside of Japan actually declines in the forecast. I guess we will see, but my impression is it is being lowballed after the experience of this year.

We won't actually know until the end of 2024 though, given that the strongest releases are from September onwards. Personally, I am happy with the strategic decisions, and the outlook numbers seem prudent this time. And let's see if there are surprises along the way!

A note on this. In the sale of Relic, and in all other restructuring efforts, not all costs derived from restructuring have been recorded under extraordinary losses. Many have been recorder as COGS when related to already launched games and so on (depreciation of games included in the sale and some restructuring costs in Creative Assembly, etc.). That means that many (in the case of the last round, about half) of the costs of the restructuring are included in the segment profitability already (as they should!)

I still think there is an element of sandbagging in the write-downs of inventory this quarter, but that's different.

2, 4, 23 and 25, at the moment.

About because there are a few things I am not entirely sure about in the cash flow statement, and I would rather read the annual report notes to see how to classify them exactly. In any case, the change would be relatively minor, and my doubts are on the proceeds from sales of shares of subsidiaries (which is negative, so it doesn't seem to match) and the Purchase of stocks of subsidiaries and affiliates (which I suspect is investing in joint ventures, but I would like to confirm!). In case all of those are effectively purchasing/selling new societies and are excluded from the FCF calculation (I usually exclude M&A, at least for most companies) it would be close to 50. If they have to be included as CAPEX, it would still be above 40. And yes, this includes the other segment in financing activities.

GAN's acquisition only makes sense to me as a gateway to sell the slot machines. If they overfocus on the online/content providing part, I think they just have no advantage there.