Quick update: Mandarake, IG Port, Gravity

Mandarake and IG Port have published new sets of results, let's review them!

Mandarake: where is my operating leverage?

I have to confess I am no longer long Mandarake. Their sales evolution until April was really good, but the last few months have been fairly disappointing. I guess I overestimated their capacity of selling out of the existing stores and, especially, their traction online.

But the most worrying part is not that, but the margins in their Q3 (until June). Basically, in Q3 they obtained the same results in terms of profit as in Q3 last year, despite more than 10% increase in sales. That contradicts the trend in the last few years, and combined with the drop in sales has convinced me to drop it.

Now, the detailed version of the results is not out yet, so I still don't know the exact cause of the drop in margins. There was a slight gross margin reduction, but also an increased expense at the corporate level that I would like more details on (I know they started to look for more inventory, if that is the root cause, it might not be that bad)

I will still keep an eye on it in the coming quarters to see if this was only a temporary misstep, as this is still an interesting area, but the core thesis was operating leverage on a sustained increase in sales, and both key areas for it have not gone well, so time to cut!

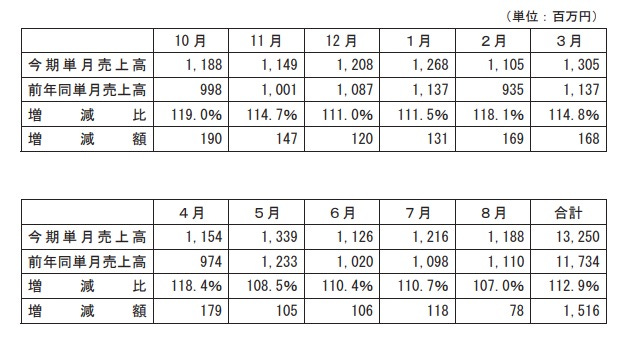

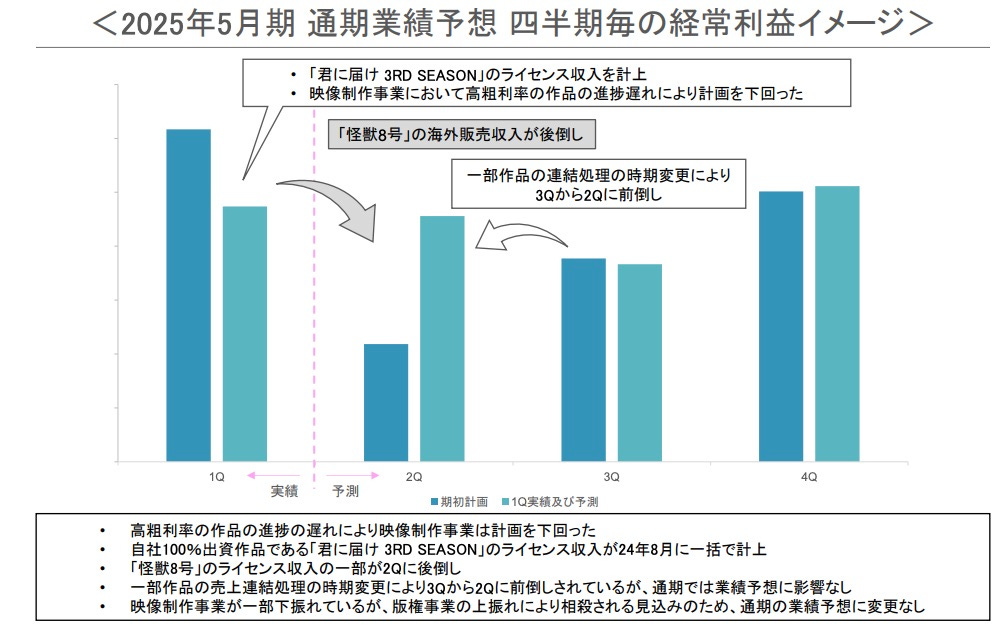

IG Port: Justified drop?

IG Port dropped almost 10% after publishing its latest set of results, although it has already recovered part of that fall. The key is that the profit was lower than expected, according to management due to a shift on the recognition on some revenue to Q2

I am inclined to believe them, as the main shift seems to come from Kaiju no. 8 overseas revenue recognition, and that is going fairly well, as far as I can tell, being one of the most popular animes in the season (although not an outsized success). Most of their other properties seem to be doing well too, and finally we have confirmation of a new Spy x Family season. Suicide Squad Isekai is doing rather poorly though (not unexpected, I must say). I don't think they were part of the production committee there, but I also don't think they made a lot of money.

The pure video production business keeps generating losses ( fairly usual in anime, but so common of late for IG Port that makes me think their investment committee partners are taking advantage of their appetite to invest in interesting properties), but copyright more than makes up for it. Despite the relative failure, operating profit is more than 30% higher than the same quarter last year.

Net profit is down though, due to the lack of investment portfolio gains and a much higher tax rate. Net profit last year was a bit overstated due to the investment portfolio results and the payment to move The Ancient Magus Bride away from Mag Garden. Effective tax rate right now is a bit too high coming, I suspect, from the fact that the animation segment is loss-making, and those loses not being compensated in the other businesses due to the structure of the group1. I hope they manage to get a better treatment in that regard eventually, or better yet, get the animation segment to stop losing money.

In any case, both revenue and operating profit go the right way, and I am pretty optimistic regarding the future of IG Port seeing that the revenue from existing properties holds quite well.

Gravity: activist incoming?

Gravity's latest set of results was disappointing, as there was no revenue from China. That was unexpected for many, and raises questions about the licensing deal they have there, given the recent releases. That sent the shares tumbling down back in August.

But as I have mentioned in prior entries, I don't think business performance is the key, although AppInvestor did a nice review of that side in his substack. The key is GungHo needing cash or perceiving they are running out of time for strategic operations (like a take under). That, or an activist fund getting involved. In that regard:

Gravity's share of the consolidated cash of the group stands now at about 41%, up from 36% at the beginning of the year, or 27% at the beginning of 2023.

An activist (Strategic Capital) has purchased 5.5% of GungHo, becoming the second largest shareholder of the group behind Taizo Son (yes, he is the brother of Softbank's Son).

I would be surprised if we don't hear more about Gravity in the coming months.

Years with higher effective tax rate typically coincide with years of losses in the animation business. See 2022. There are different companies and some minority interests involved, which complicates more rational set-ups.